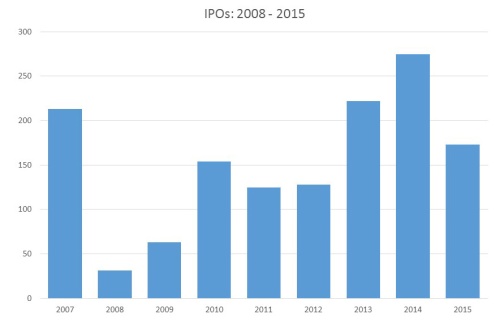

As reported in the WSJ’s optimistically titled article Flurry of IPOs Poised to Test Market for New Offerings, “the IPO market is perking up after the slowest year for new U.S. listings in more than a decade. Nine companies began to pitch their initial public offerings to prospective investors so far this week. That is the most since 13 did so in one week in June 2015.”

Our transaction team is experiencing this optimism and has been actively counseling pre-IPO companies through the S-1 draft registration process. THIS WHITEPAPER is a core (and illustrative) document for that.

Our transaction team is experiencing this optimism and has been actively counseling pre-IPO companies through the S-1 draft registration process. THIS WHITEPAPER is a core (and illustrative) document for that.

But even before the drafting, our conversations revolve around converting from a private company into a public company… and extremely burdensome for your accounting team… soon to rebranding as “your financial reporting department,” BTW. Often, the process of converting to public company financial statements is long and complex, and can reveal unexpected challenges. Allowing sufficient preparation time for this process is important. Commencement of this process as soon as an IPO becomes an optional strategy for the company is recommended.

Mike Gould, Partner at PwC explains in this video snippet.

Giving your financial teams ample time to prepare AND learn the IPO financial vocabulary is key as they will be responsible for the documentation of critical and judgmental accounting policies related to all the financial statements.

- Revisiting/enhancement of accounting policies in footnotes

- Incremental disclosures to comply with SOX e.g., segments, earnings per share (EPS), pro forma info for business combinations

- Preparation of documentation in anticipation of SEC comments

- Increased attention on auditor independence, requiring company to prepare its own documentation of key accounting policies

For more depth, watch the complete IPO webinar HERE.

c

A look at EY’s

A look at EY’s